Life can be unpredictable. Unexpected events can happen at any time. A life insurance policy ensures that your family remains financially stable if something happens to you. It covers expenses like funeral costs, debts, and living expenses. This support can be crucial during tough times.

In this blog post, we will explore the different types of life insurance policies. We will also discuss their benefits and how to choose the right one. By understanding these options, you can make an informed decision that best suits your needs and provides security for your family. So, let’s dive in and learn more about life insurance policies.

Introduction To Life Insurance

Life insurance is essential for financial planning. It provides security and peace of mind. Knowing about life insurance can help you make informed decisions for your family’s future.

Importance Of Life Insurance

Life insurance is crucial for protecting loved ones. It helps cover funeral expenses and outstanding debts. Your family can maintain their lifestyle even if you’re gone. Life insurance can also help with your children’s education costs. It ensures your dependents are not burdened financially.

Basic Concepts

Life insurance is a contract between you and an insurer. You pay regular premiums. In return, the insurer pays a lump sum to your beneficiaries. There are two main types: term life and whole life insurance. Term life covers you for a specific period. Whole life provides coverage for your entire life.

Premiums are based on factors like age, health, and coverage amount. The younger and healthier you are, the lower your premiums. It’s important to review your policy regularly. Make sure it still meets your needs.

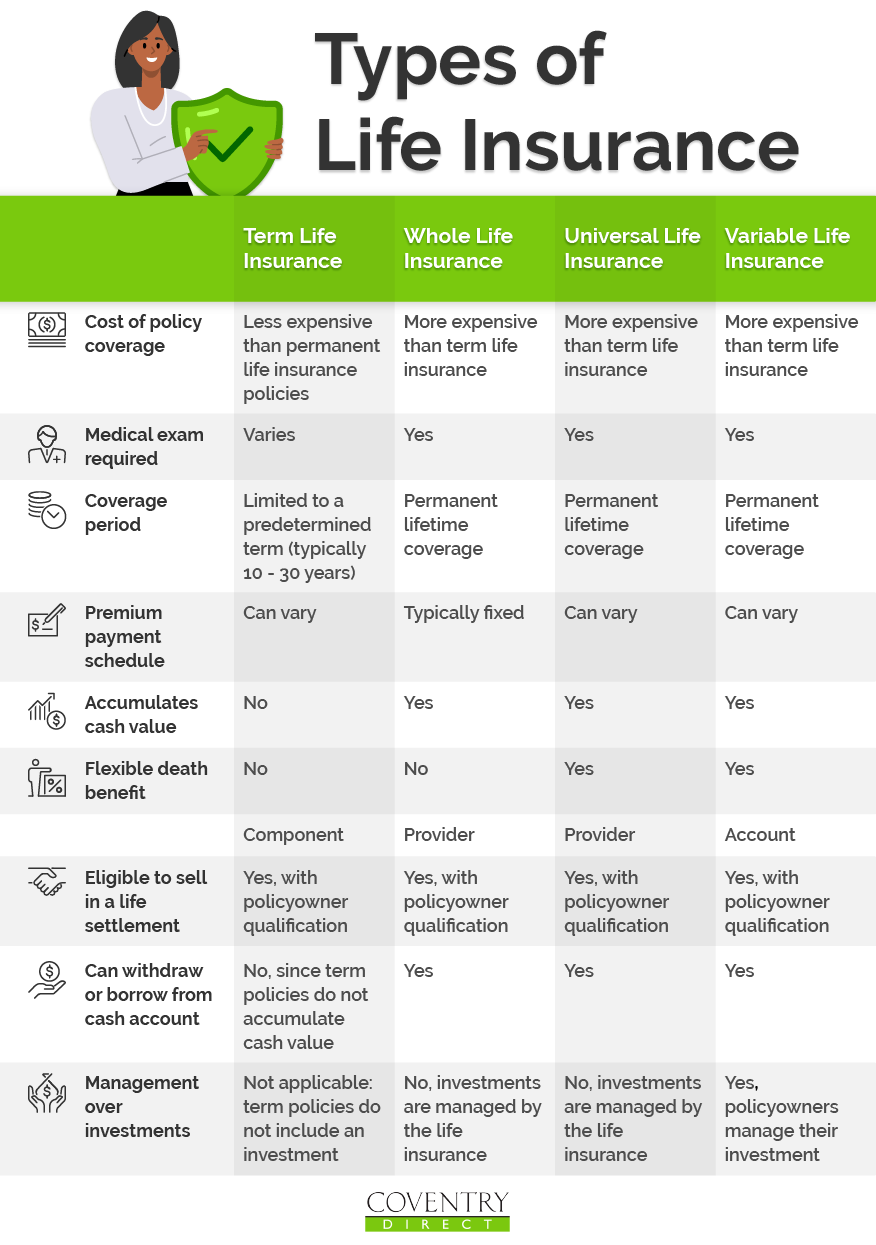

Types Of Life Insurance Policies

Understanding the types of life insurance policies can help you make informed decisions. Different policies offer various benefits. Knowing these can ensure you choose the right one for your needs.

Term Life Insurance

Term life insurance covers you for a specific period. This can be 10, 20, or 30 years. If you pass away during this term, your beneficiaries receive a death benefit. This type is usually less expensive. It does not build cash value. It’s ideal for covering short-term needs.

Whole Life Insurance

Whole life insurance provides coverage for your entire life. It has a fixed premium. This means your payments stay the same. It also builds cash value over time. You can borrow against this value. This type can be more expensive. It offers lifelong protection and savings.

Universal Life Insurance

Universal life insurance is flexible. It allows you to adjust your premiums. You can also change the death benefit. It builds cash value, like whole life insurance. The cash value can earn interest. This type offers more control. It can adapt to your changing needs.

Benefits Of Life Insurance

Life insurance offers many benefits for you and your loved ones. It ensures your family’s future and provides financial support in tough times. Let’s explore some key advantages of having a life insurance policy.

Financial Security

Financial security is one of the main benefits of life insurance. In the event of your passing, your family will have the funds they need. This can help cover daily expenses, mortgage payments, and other financial obligations.

| Expense Type | Life Insurance Coverage |

|---|---|

| Daily Living Costs | Yes |

| Mortgage Payments | Yes |

| Children’s Education | Yes |

| Debt Repayment | Yes |

Tax Advantages

Life insurance policies come with significant tax advantages. The death benefit your beneficiaries receive is usually tax-free. This means they get the full amount of the policy without tax deductions. Also, some policies offer tax-deferred growth of cash value.

- Death benefits are generally tax-free.

- Cash value grows tax-deferred.

Wealth Transfer

Life insurance is a useful tool for wealth transfer. It ensures that your assets are passed on to the next generation smoothly. Your beneficiaries receive the policy payout without dealing with probate court. This can save time and reduce stress during an already difficult period.

- Smooth asset transfer

- Avoid probate court

- Reduce stress for beneficiaries

Credit: illinoislawforyou.com

Choosing The Right Policy

Life insurance is a crucial part of financial planning. Choosing the right policy can be challenging. It’s important to find a policy that meets your needs. Here’s a guide to help you make an informed decision.

Assessing Your Needs

Begin by assessing your needs. Consider the following factors:

- Your age

- Health condition

- Financial obligations

- Number of dependents

- Future goals

Estimate the amount of coverage you need. This will depend on your current and future expenses. Include mortgage payments, education costs, and daily living expenses. A clear understanding of your needs will help you choose the right policy.

Comparing Different Policies

Once you know your needs, compare different policies. Here are some types of life insurance policies:

| Policy Type | Description |

|---|---|

| Term Life Insurance | Offers coverage for a specific period. It’s usually less expensive. |

| Whole Life Insurance | Provides coverage for your entire life. It includes a savings component. |

| Universal Life Insurance | A flexible policy with investment options. It allows for adjustable premiums and benefits. |

Compare the benefits and costs of each policy. Look at the premium amounts, coverage terms, and additional features. Make sure the policy fits your budget and meets your financial goals.

Choosing the right life insurance policy requires careful consideration. Assess your needs and compare different policies. This will help you make a well-informed decision.

Cost Of Life Insurance

The cost of life insurance can vary greatly. Many factors influence the premiums you pay. Understanding these factors can help you make informed choices. Let’s explore what affects the cost and how you can lower it.

Factors Affecting Premiums

Several elements impact the cost of your life insurance. Your age plays a big role. Younger people usually pay less. Health is another key factor. Healthy individuals get better rates. Smoking can increase your premiums. Your occupation matters too. Dangerous jobs mean higher costs. The type of policy you choose also affects the price. Term policies often cost less than whole life policies.

Ways To Lower Costs

There are ways to reduce your life insurance expenses. Maintain a healthy lifestyle. Regular exercise and a good diet help. Avoid smoking and limit alcohol. Shop around for the best rates. Compare different companies and policies. Consider a term policy if you need lower premiums. Review your coverage needs regularly. Adjust your policy as your situation changes. Paying premiums annually instead of monthly can save money.

Policy Riders And Add-ons

Life insurance policies can be customized with policy riders and add-ons. These options allow you to tailor your policy to fit your unique needs. Riders and add-ons provide extra benefits and coverage, enhancing your policy’s value and flexibility.

Common Riders

Here are some of the most common riders you can add to your life insurance policy:

- Accidental Death Benefit Rider: Provides an extra payout if death is due to an accident.

- Waiver of Premium Rider: Waives premiums if you become totally disabled.

- Critical Illness Rider: Pays a lump sum if diagnosed with a critical illness.

- Child Term Rider: Provides term life insurance for your children.

- Long-Term Care Rider: Covers costs for long-term care services.

Benefits Of Add-ons

Adding riders to your policy offers several benefits:

- Increased Coverage: Enhance your policy’s coverage without buying a new policy.

- Flexibility: Customize your policy to meet changing needs.

- Cost-Effective: Often cheaper than purchasing separate policies.

- Peace of Mind: Provides extra security and assurance.

Here’s a quick comparison of some common riders:

| Rider | Benefit | Cost |

|---|---|---|

| Accidental Death Benefit | Extra payout for accidental death | Low to Moderate |

| Waiver of Premium | Premiums waived if disabled | Low |

| Critical Illness | Lump sum for critical illness | Moderate |

| Child Term | Term insurance for children | Low |

| Long-Term Care | Covers long-term care costs | High |

Policy riders and add-ons make your life insurance policy more robust. They provide added protection and peace of mind.

How To Apply For Life Insurance

Applying for a life insurance policy can seem daunting. But with the right guidance, it becomes much simpler. This section will walk you through the steps to apply for life insurance.

Application Process

The first step in the process is choosing the right policy. Research different plans and select one that suits your needs. You can do this online or speak with an insurance agent.

Once you have selected a policy, gather the necessary documents. These usually include:

- Identification proof (e.g., passport, driver’s license)

- Proof of address (e.g., utility bills, lease agreement)

- Financial documents (e.g., bank statements, income proof)

Next, fill out the application form. This can often be done online. Provide accurate and honest information. Your form will ask about your personal details, health history, and lifestyle.

After submitting your form, the insurance company will review it. They might ask for additional information or documents. Be prompt in your responses to avoid delays.

Medical Examination

Most life insurance policies require a medical examination. This helps the insurer assess your health risks.

The exam usually includes:

- Basic health check (e.g., height, weight, blood pressure)

- Blood tests

- Urine tests

The insurer may also ask about your medical history. This could include past illnesses, surgeries, and family health history.

Prepare for the medical exam by getting a good night’s sleep. Avoid alcohol and caffeine before the test. Follow any instructions given by the insurance company.

After the exam, the results are sent to the insurer. They will use this information to determine your premium rates and policy approval.

Applying for a life insurance policy is straightforward. Follow these steps to secure your financial future.

Maintaining Your Policy

Maintaining your life insurance policy ensures it remains effective and relevant. Regular reviews and updates help you stay protected. Below are key steps to maintain your policy.

Regular Reviews

Regular reviews of your life insurance policy are crucial. They help you assess whether your coverage still aligns with your needs. Life changes, such as marriage or having children, may require more coverage. Reviewing your policy ensures you have adequate protection.

Here are some tips for regular reviews:

- Review your policy annually.

- Check if the coverage amount meets your current needs.

- Evaluate any changes in your health or lifestyle.

Updating Beneficiaries

Updating beneficiaries on your life insurance policy is essential. Ensure the right individuals benefit from your policy. Life events, such as marriage, divorce, or having children, may necessitate changes.

Steps to update beneficiaries:

- Contact your insurance provider.

- Submit a change of beneficiary form.

- Confirm the update with your provider.

Keep your beneficiaries’ contact information current. This helps in the swift processing of claims.

Common Myths And Misconceptions

Life insurance is a crucial part of financial planning. Yet, many people have misconceptions about it. These myths can prevent individuals from getting the protection they need. Let’s debunk some of the most common myths and misconceptions.

Life Insurance Is Expensive

Many believe that life insurance is costly. This is not always true. There are different types of policies available. Some are affordable for most budgets.

A term life insurance policy can be very affordable. The cost depends on factors like age, health, and coverage amount. For young and healthy individuals, premiums can be as low as a few dollars a month.

Here is a simple comparison table for monthly premiums:

| Age | Monthly Premium |

|---|---|

| 25 | $10 |

| 35 | $15 |

| 45 | $25 |

As you can see, the cost can be quite manageable. It is important to shop around and compare different policies.

Only Breadwinners Need Coverage

Another common myth is that only the primary earner needs life insurance. This is not true. Non-working spouses and stay-at-home parents also contribute significantly to the household.

Consider the value of childcare, housekeeping, and other services they provide. If something happens to them, the family might face financial strain.

Here are some reasons why stay-at-home parents need coverage:

- Childcare costs

- Household management

- Future education expenses

Life insurance can help cover these costs. It ensures that the family can maintain their lifestyle even after a loss.

In short, everyone in the family should be considered when it comes to life insurance.

By understanding the truth behind these myths, you can make better decisions about life insurance. Protect your loved ones and secure your financial future.

Credit: fidelitylife.com

Credit: www.coventrydirect.com

Frequently Asked Questions

What Is A Life Insurance Policy?

A life insurance policy is a contract. It pays a lump sum to beneficiaries upon the policyholder’s death. It provides financial security.

How Does Life Insurance Work?

Life insurance works by paying premiums. In exchange, the insurer pays a benefit to the beneficiaries after the policyholder’s death.

Why Should I Buy Life Insurance?

Buying life insurance ensures financial security. It helps cover expenses like debts, funeral costs, and living expenses for loved ones.

What Are The Types Of Life Insurance?

There are two main types: term life insurance and whole life insurance. Term covers a specific period, while whole life covers the policyholder’s entire life.

Conclusion

A life insurance policy offers peace of mind and financial security. It protects your loved ones when you are gone. Choosing the right policy can be confusing. But it is an important decision for your family’s future. Take your time to compare options and ask questions.

Make sure you understand the terms fully. Investing in a life insurance policy today secures your family’s tomorrow. Your loved ones will thank you for it.